With the national average 30-year fixed refinance rate hovering around 6.81%, refinancing could be worth a closer look. This is especially if you bought your home after the pandemic, when interest rates peaked around 7.7% or higher. In many cases, lowering your rate by just 0.75 percentage points can make a noticeable difference in your monthly payments and long-term savings.

Whether you're looking to reduce your payments, shorten your loan term or access home equity, refinancing may offer a path forward. Read on to learn the ins and outs of mortgage refinancing so you can make the right financial decision for your situation.

What Is Mortgage Refinancing?

Refinancing a mortgage means replacing your current home loan with a new one, often with different terms, a new interest rate or both. When you refinance, your original mortgage is paid off, and you begin a new loan agreement.

There are several common reasons homeowners consider refinancing their mortgage:

- To lower monthly payments by securing a lower interest rate.

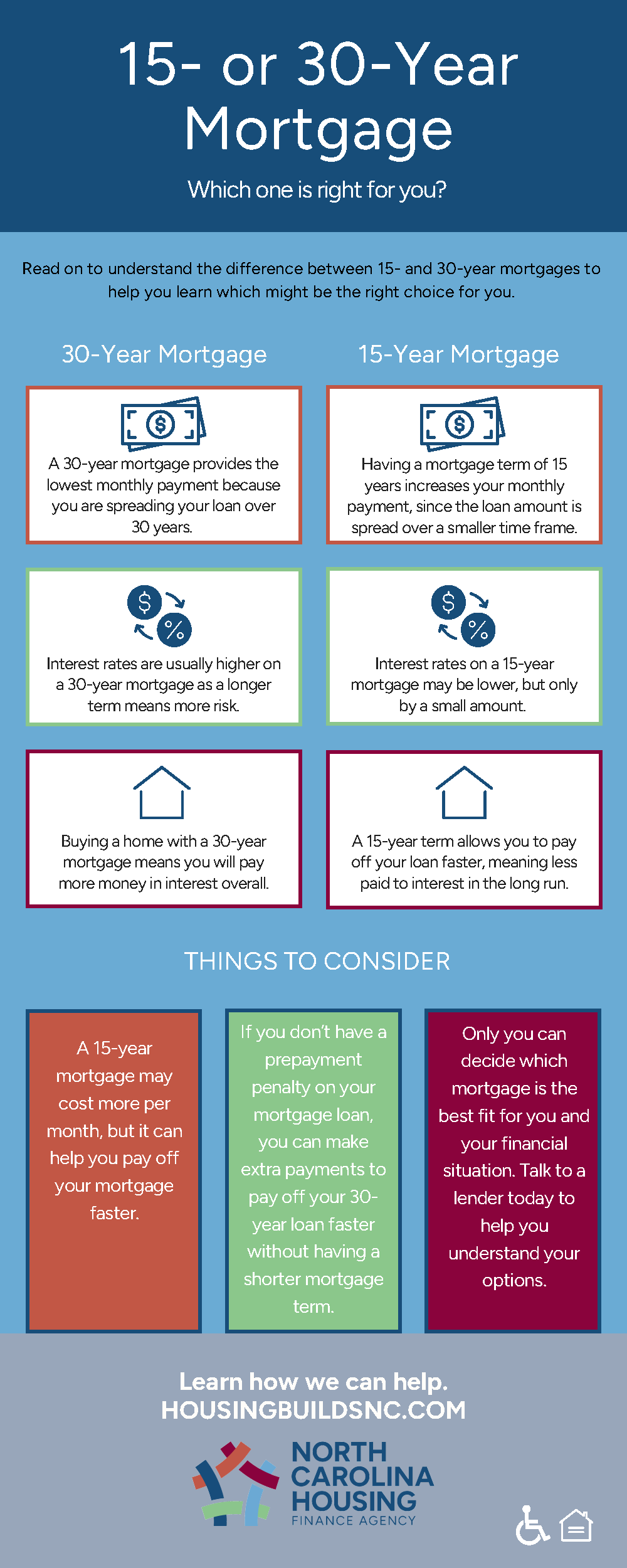

- To shorten the loan term (e.g., from 30 to 15 years) in order to build equity faster and save on interest over time.

- To switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for more predictable payments.

- To eliminate private mortgage insurance (PMI) by increasing home equity through a cash-in refinance.

- To use a cash-out refinance to access home equity for renovations, debt repayment or other financial needs.

{kind=link}

Even if rates haven’t dropped significantly, refinancing may still be beneficial if your financial goals or situation have changed.

Is Refinancing Right for You?

Deciding whether to refinance depends on your unique financial picture. Here are some signs it might make sense for you to talk to your lender or financial advisor about refinancing:

- You qualify for a significantly lower rate than your original mortgage.

- You want to reduce your monthly payment and extend your loan term.

- You have an ARM and want the stability of a fixed-rate loan.

- You want to pay off your mortgage sooner and are prepared for a higher monthly payment.

- You’ve built equity in your home and want to put it to work through a cash-out refinance.

As always, consult with your lender or a financial advisor to determine whether refinancing aligns with your long-term goals.

The North Carolina Housing Finance Agency offers resources for home buyers across North Carolina, including a list of our preferred lenders. For more information about the home buying process, affordable mortgage options and more, visit www.HousingBuildsNC.com.

For more information on refinancing, check out this guide from the Consumer Financial Protection Bureau.