Affordable housing is a cornerstone of economic resilience, and in North Carolina, the Low-Income Housing Tax Credit (“LIHTC” or “Housing Credit”) has been one of the strongest—and largest—financing tools for creating and rehabilitating affordable rental homes across the state. For nearly four decades, the North Carolina Housing Finance Agency has used Housing Credits to help ensure that families with modest income can find—and keep—safe, stable and affordable places to live.

From 1987 through September 2025, the Housing Credit has helped create and preserve 121,950 affordable apartments in 2,702 properties across North Carolina. In exchange for these tax credits, owners agree to rent restrictions intended to ensure homes are affordable for low-income residents. Generally, these restrictions last for 30 years and the Agency monitors them closely for compliance. For tenants, it means predictability and protection from large rent increases—at least for as long as the affordability restrictions remain in place.

And that’s the challenge: rent restrictions do not last forever. Once a Housing Credit-financed property reaches the end of its required affordability term, it may remain affordable or reposition as market-rate housing. Research has found that several factors influence whether a Housing Credit property continues to operate as affordable housing or converts to market-rate housing, including the local housing market, the physical and financial condition of the property, property ownership, ability to recapitalize and presence of subsidies with additional affordability restrictions[i]. As the Housing Credit program matures and the 30-year affordability requirements for the early generation of properties continue to reach their expiration, understanding this pivotal transition becomes increasingly important.

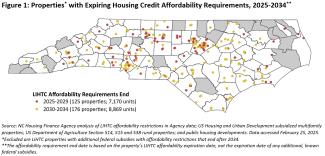

Within the next decade, 16,000 affordable apartments across North Carolina could lose their affordability restrictions if no additional preservation efforts are made, according to a new Agency white paper released this week. This includes a mixture of rural and urban properties, from small-town complexes with just a few dozen apartments to large, multi-building communities in the state’s larger cities.

The good news is there are proven strategies to keep these homes affordable. Strong data tracking helps identify at-risk properties early, making it easier to target preservation resources—whether it’s a new allocation of Housing Credits to address the property’s rehabilitation needs or additional local, state, or federal subsidies with affordability restrictions to keep rents low. In the last three years alone, 75 properties (2,562 units) have seen their Housing Credit affordability restrictions expire. Of these, 5 properties (121 units) have recapitalized with a new allocation of Housing Credits in the last three years, which triggers a new 30-year affordability period; 5 properties (194 units) have an additional Agency loan that was extended or still governing affordability; and 44 properties (1,343 units) still have active affordability restrictions from a known federal subsidy. The remaining 21 properties (927 units) have seen their Housing Credit affordability expire without these other mechanisms to maintain rent affordability.

As the state’s LIHTC portfolio matures, the expiration of affordability requirements presents both opportunities and challenges. The Housing Credit has a long history of creating—and preserving—safe, stable affordable housing for North Carolinians. The challenges are real, but so are the tools to meet it.

Read the full white paper here.

------------

[i] See, for example: PAHRC and NLIHC. (2024) “2024 Picture of Preservation.” Available from: https://preservationdatabase.org/picture-of-preservation/; Meléndez, E., Schwartz, A.F., & Montrichard, A.D. (2008). “Year 15 and Preservation of Tax-Credit Housing for Low-Income Households: An Assessment of Risk.” Housing Studies, 23, 67-87.